Business Strategy & Competitive Advantages: Business Strategy

Our long-term financial strategy for creating shareholder value

At Travelers, our simple and unwavering mission for creating shareholder value is as follows:

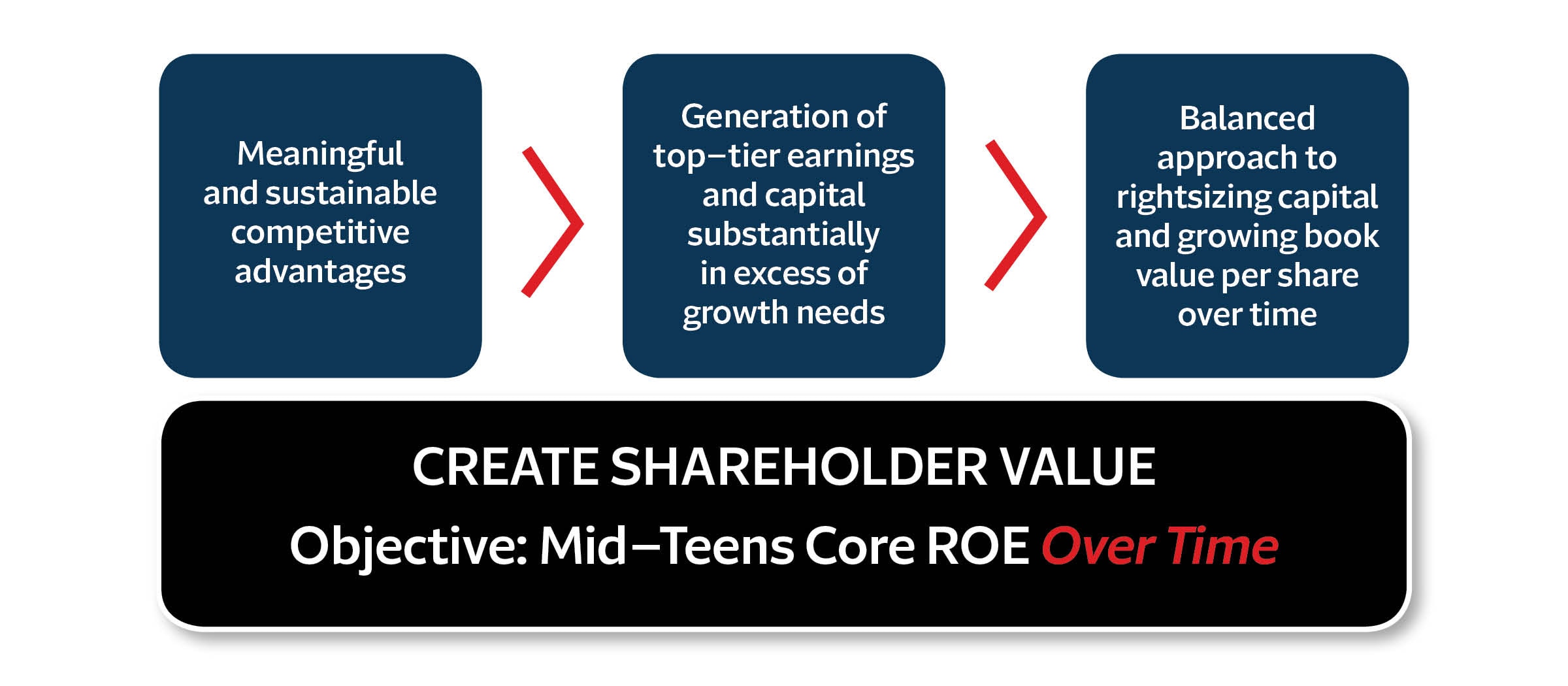

Business Strategy flowchart. Our Long-Term Financial Strategy for Creating Shareholder Value. Travelers creates shareholder value over time through meaningful and sustainable competitive advantages; generation of top-tier earnings and capital substantially in excess of growth needs; and a balanced approach to rightsizing capital and growing book value per share over time.

Delivering industry-leading return on equity over time

The results we deliver are due to our deliberate and consistent approach to creating shareholder value. We have been clear for many years that one of our crucial responsibilities is to produce an appropriate return on equity for our shareholders. This has meant developing and executing financial and operational plans consistent with our goal of achieving superior returns, which we defined many years ago as a mid-teens core return on equity over time. We emphasize that this objective is measured over time because we recognize that the macroeconomic environment, loss cost trends, weather and geopolitical and other factors impact our results from year to year, and that there will be years – or longer periods – in which industry-leading returns are either above or below mid-teens depending on the environment. In any event, we seek to generate industry-leading returns that are meaningfully above the risk-free rate and our cost of equity.

Our focus on core return on equity encompasses multiple performance objectives key to creating shareholder value. The measure is a function of both core income and shareholders’ equity (excluding unrealized gains and losses on investments). Accordingly, core return on equity reflects a number of separate areas of financial performance related to both our income statement and balance sheet, including the quality and profitability of our underwriting and investment decisions, the pricing of our policies, the effectiveness of our claim management and the efficacy of our capital and risk management.

Our data-driven underwriting culture and expertise

Underwriting excellence is, of course, key to our success, and there is nothing more critical to underwriting excellence than a culture that values strong performance over time and understands how to balance the art and science of decision making.

In that regard, our culture alone is a significant and sustainable competitive advantage. In our commercial businesses, that means granular execution on an account-by-account or class-by-class basis. In personal lines, it means a very high degree of segmentation by risk profile, product and geography. With that and our advanced analytical capabilities, we thoughtfully select the risks that we write and price our products deliberately with our target return in mind.

Like every aspect of our business, our focus on performance over time is core to how we manage our catastrophe exposure. Although we are unable to predict what the next event will be or where it will occur, we take steps every day to ensure that our portfolio of risk properly contemplates the potential for loss and that we maintain the right balance of risk and reward.

Due to our disciplined approach to catastrophe management, our share of catastrophe losses over time has been significantly favorable relative to our market share. This outperformance is the result of our prudent and integrated approach to managing our catastrophe exposures through portfolio, risk selection, underwriting and pricing actions.

We continue to make significant investments in advanced capabilities to ensure that our catastrophe management teams and underwriters have the tools and insights necessary to develop a comprehensive view of catastrophe risk. We believe that these investments position Travelers to continue to outperform.

Another pillar of our underwriting strength is a deliberate approach to reinsurance. The quality of our underwriting and the diversification of our business allow us to seek to optimize the portion of our business that we cede to reinsurers. While reinsurance remains an important tool for managing balance sheet risk and volatility, it comes at a cost, as reinsurers must earn an appropriate return on the capital they deploy.

With that in mind, we generally prefer to retain a high percentage of the economics of the business we write. Our deep expertise across the broad suite of products we offer, coupled with our scale and long-standing reputation for underwriting discipline, makes us a highly valued counterparty in the reinsurance market. That standing affords us flexibility. When market conditions are favorable, we have the ability to purchase added coverage on attractive terms. When they are not, we have the ability to retain more risk on our own balance sheet.

A deliberate and data-based approach to reserving and a healthy appreciation of risk

Our reserving is the result of a consistent, disciplined culture – one that has a healthy respect for uncertainty and a commitment to responding appropriately to emerging data. The loss environment has changed considerably over the past two decades, and not always in ways that were easy to anticipate. The rates at which claimants choose to be represented by attorneys have climbed significantly. Nuclear verdicts have become more frequent and more severe. Third-party litigation finance has become a significant asset class. Inflation surged unexpectedly in the post-COVID period. And emerging liabilities have reshaped the industry’s loss landscape – from changes in laws allowing the revival of previously time-barred claims to mass tort actions relating to opioids, PFAS, talc and more.

Our reserve position is not just the output of our models – it is the people and the processes behind them. Business leaders, underwriters, actuaries, finance leaders and Claim professionals sit together and rigorously examine the data, challenge assumptions and test conclusions. That culture of individual and collective accountability and disciplined analysis has allowed Travelers to consistently recognize and respond to trends earlier than most in our industry.

An early and accurate view of the loss environment is not just a balance sheet exercise – it is a competitive advantage. It gives us an edge in risk selection, pricing segmentation and claim strategy, and it will continue to differentiate us in the years ahead.

Disciplined investment approach

Much like our underwriting strategy, successfully balancing risk and reward is at the heart of our well-defined investment philosophy. We strive to be thoughtful underwriters on both sides of the balance sheet, and we have always managed our investment portfolio to support our insurance operations, not the other way around. Accordingly, our investment portfolio is positioned to meet our obligations to policyholders under almost every foreseeable circumstance – anything from a financial crisis to a global pandemic to a significant natural disaster. With this in mind, we are focused on risk-adjusted returns and credit quality rather than reaching for yield that is not commensurate with the underlying risk. In addition, our Investment Policy, approved by our Board of Directors, reflects a long-term approach to sustainable value creation.

Travelers’ powerful earnings engine

Our competitive advantages set us apart; they are foundational to the success of our long-term financial strategy. At the same time, we understand clearly that the world is changing, and changing quickly. Recognizing that any strategy to deliver leading return on equity over time requires a strategy to grow over time, about 10 years ago, we embarked on a strategy to achieve profitable growth in the context of the forces of change identified as impacting the industry. Broadly speaking, we see four significant forces of change impacting our industry:

- Consumers’ expectations are changing and being shaped by their experiences in other industries.

- Rapid progress in technology is enabling us to reimagine almost every aspect of our business.

- The opportunities presented by data and analytics are transforming every aspect of our business.

- Traditional distribution is consolidating and alternative models are developing.

Core to this strategy was executing on an ambitious innovation agenda to leverage those forces of change. As those forces of change have evolved since then, we have methodically, iteratively and deliberately evolved this strategy. That is the focus of our innovation agenda: making sure that our competitive advantages are as relevant and differentiating tomorrow as they are today.

Ultimately, the vision of our innovation agenda is to be:

The undeniable choice for the customer and an indispensable partner for our agents and brokers.

This vision drives our three innovation priorities:

- Extending our advantage in risk expertise.

- Providing great experiences for our customers, agents and brokers, and employees.

- Optimizing our productivity and efficiency.

A key theme running through our investments is that they are designed in large part to enable us to optimize the top line at attractive returns. We have been investing in these priorities for several years while delivering industry-leading returns and an improving expense ratio.

Our successful execution of this strategy through various economic and market conditions has created a virtuous cycle, one in which the combination of well-conceived and executed strategic initiatives, an effective capital management strategy and a thoughtful investment strategy, contribute to attractive returns and growth in adjusted book value per share.

The following charts illustrate the power of our strategy at work and its compounding, multiyear benefit.

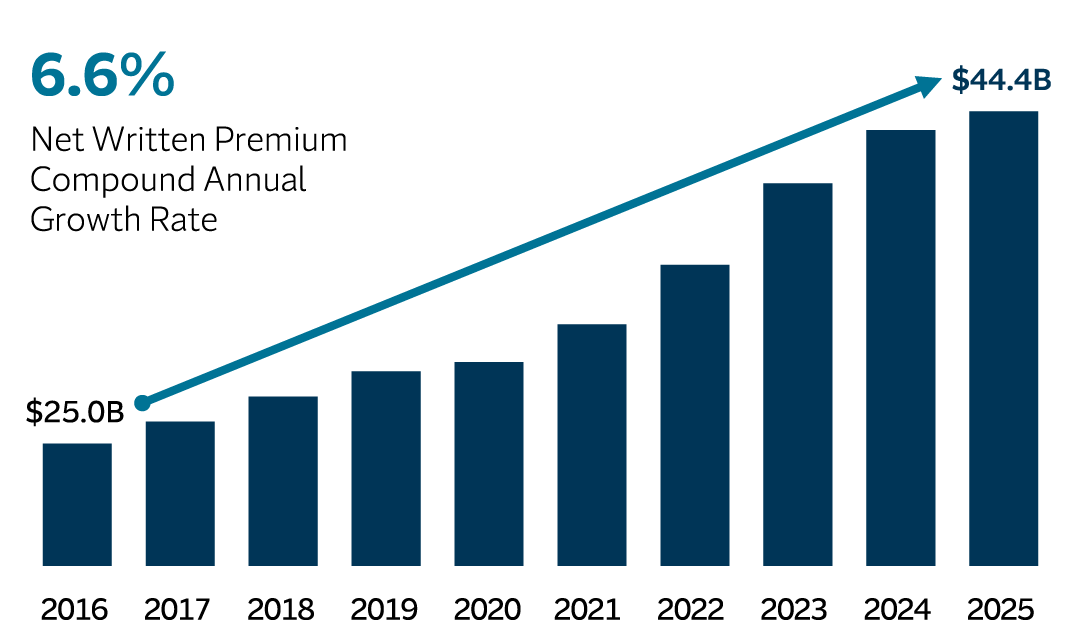

Significant net written premium growth

Bar chart displaying Significant Net Written Premium Growth from 2016 through 2025, showing an increase from $25 billion in 2016 to $44.4 billion in 2025. Compound annual growth rate (CAGR) from 2016 through 2025 was 6.6%.

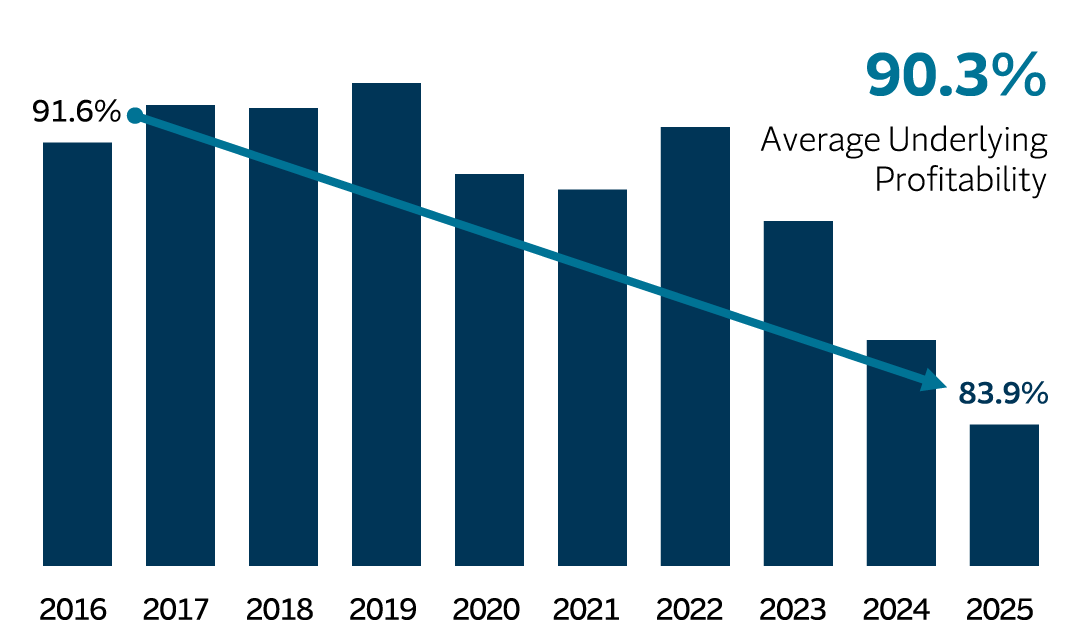

Improved underlying profitability1

Bar chart displaying Improved Underlying Profitability from 2016 through 2025. In 2025, the underlying underwriting combined ratio was 83.9%. In 2016, the underlying underwriting combined ratio was 91.6%. The average across 2016 to 2025 was 90.3%. This data excludes the impact of net prior year reserve development and catastrophe losses.

1 Underlying underwriting combined ratio, which excludes the impact of net prior year reserve development and catastrophe losses.

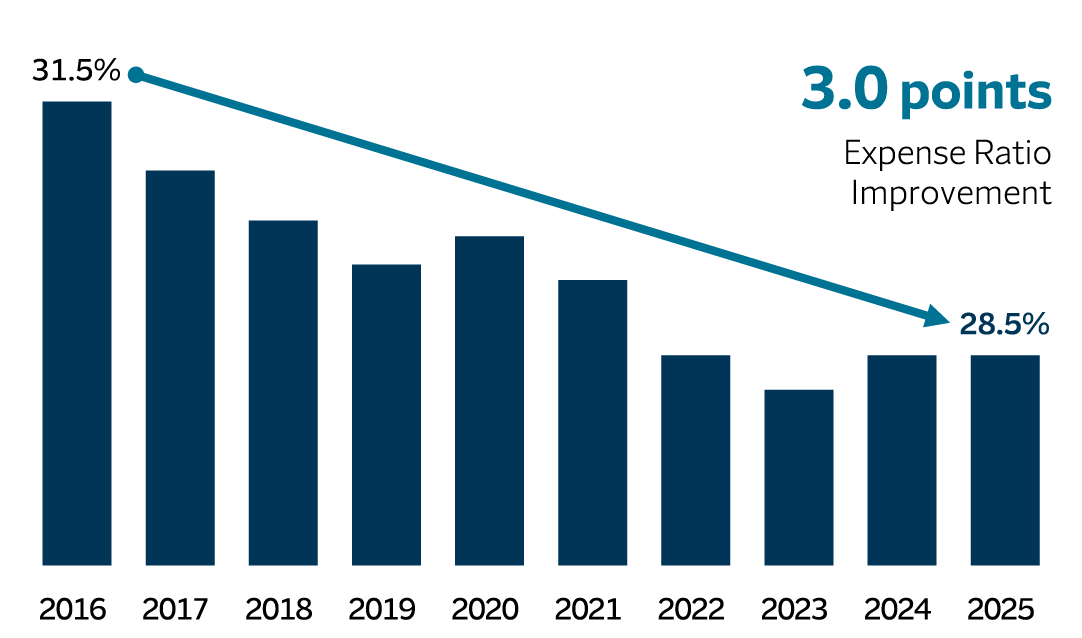

Improved expense ratio

Bar chart displaying Improved Expense Ratio from 2016 through 2025. The ratio improved 3.0 points from 31.5% in 2016 to 28.5% in 2025.

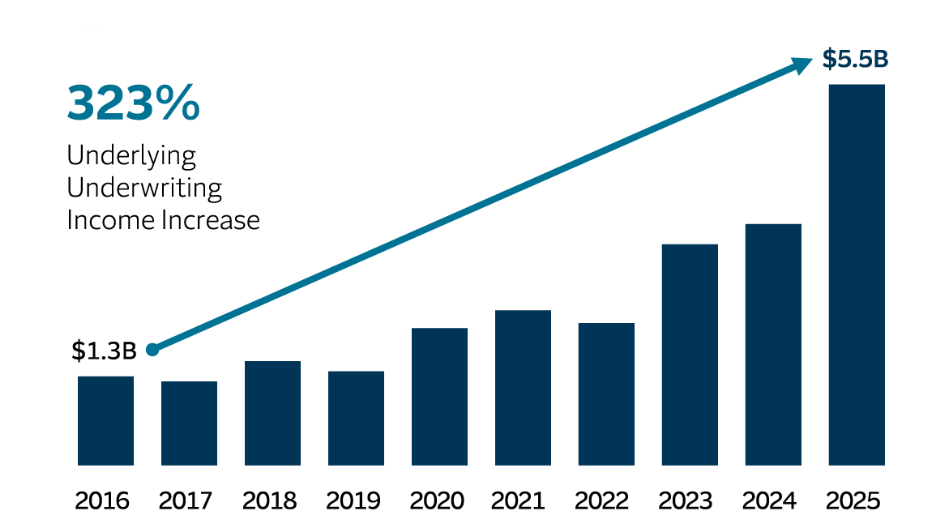

Higher underlying underwriting income2

Bar chart displaying Higher Underlying Underwriting Income from 2016 through 2025. The increase from 2016 through 2025 was 323%, representing an increase from $1.3 billion in 2016 to $5.5 billion in 2025. This data excludes the impact of net prior year reserve development and catastrophe losses.

2 Underlying underwriting income (after-tax), which excludes the impact of net prior year reserve development and catastrophe losses.

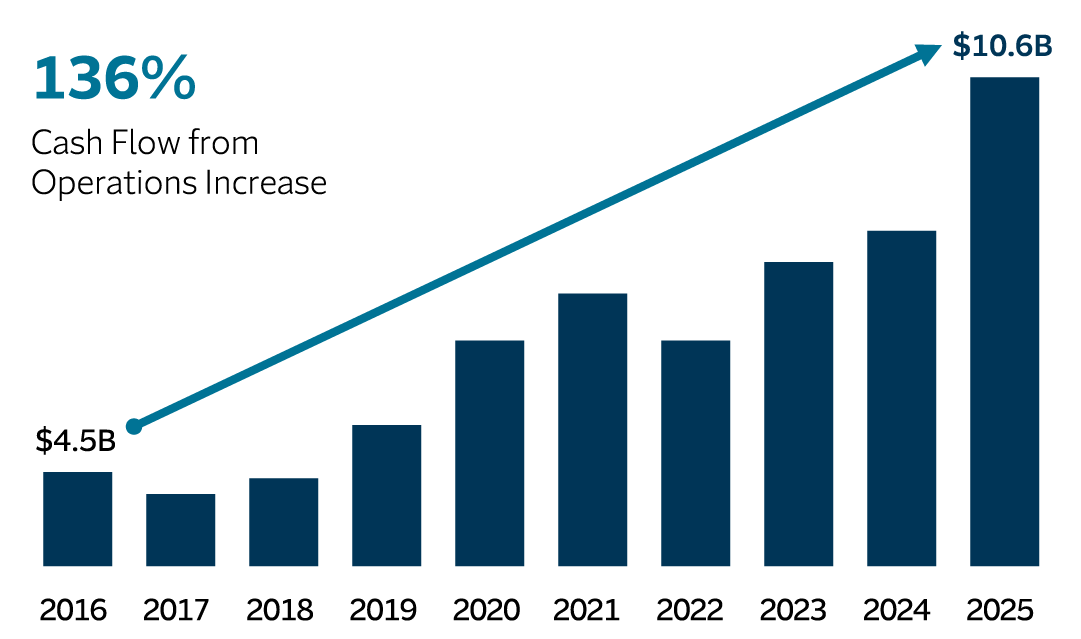

Higher cash flow from operations

Bar chart displaying Higher Cash Flow from Operations from 2016 through 2025. The increase from 2016 through 2025 was 136%, representing an increase from $4.5 billion in 2016 to $10.6 billion in 2025.

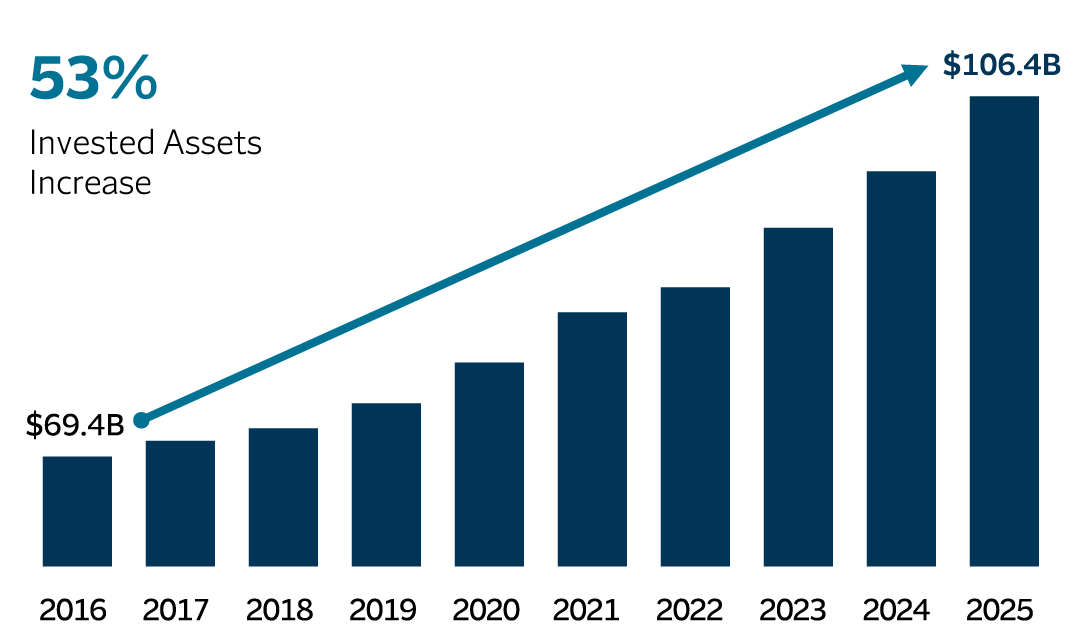

Higher invested assets3

Bar chart displaying Higher Invested Assets from 2016 through 2025. The increase from 2016 through 2025 was 53%, representing an increase from $69.4 billion in 2016 to $106.4 billion in 2025. Invested assets excludes net unrealized investment gains (losses). Invested assets includes $3.3 billion of invested assets classified as held for sale as of December 31, 2025.

3 Invested assets excludes net unrealized investment gains (losses). Invested assets includes $3.3 billion of invested assets classified as held for sale as of December 31, 2025.

We refer to this effort over the last decade as Innovation 1.0. Now, with artificial intelligence (AI) and – not too far off – quantum computing on the agenda, we are embarking on what we are calling “Innovation 2.0.”

Over the past decade, we have developed the competitive advantage of an innovation skill set. Now, we are bringing all that hard-won know-how to Innovation 2.0 at Travelers. The P&C industry is well positioned to benefit from AI across the entire value chain. This generation of AI can understand and execute on the complex stakeholder interactions, well-defined processes, data-intensive workflows and massive amounts of unstructured data that characterize our industry. The gains compound over many, many interactions. In that context, Travelers is particularly well positioned.

As an industry leader, we bring differentiating domain expertise. Because AI amplifies existing strength, leaders in the domain are best positioned to use it to drive improvement.

In addition, we have decades of high-quality data from millions of transactions and interactions and the scale to invest at significant levels as AI and technology continue to segment the market. We have thousands of engineers, data scientists and analysts building AI and other sophisticated technology solutions. Dozens of generative AI tools are already in production. Millions of transactions are now automated. More than 20,000 of our colleagues use AI tools on a regular basis, and agentic AI is not a future aspiration, it is embedded in our business operations today.

See the Non-GAAP Reconciliations section for a discussion and calculation of non-GAAP financial measures.

A balanced approach to rightsizing capital

Our capital management strategy has been an important driver of shareholder value creation. Our first objective for the capital we generate is to reinvest it in our business – organically and inorganically – to create shareholder value. For example, to the extent we continue to grow premium volumes, the level of capital to support our financial strength ratings will also increase. Also, we continue to invest in everything from talent to technology to advance our strategic objectives and power tomorrow’s performance.

Having said that, we are disciplined stewards of our shareholders’ capital. To the extent that we generate capital that we cannot reinvest consistent with our objective of generating industry-leading returns over time, we will manage it in the same way we have for decades – by returning it to our shareholders through dividends and share repurchases.

By returning excess capital to our investors, we give them the ability to allocate their investment dollars as they see fit, including by investing in companies with different growth profiles or capital needs, thereby efficiently allocating capital across the economy. That efficient allocation of capital in the marketplace contributes to a stronger economy.

Acquisitions and footprint

The lens through which we evaluate strategic opportunities is that a transaction should contribute to our mission by improving our long-term return profile, reducing the volatility of our returns or creating shareholder value through some other important strategic benefit, such as a geographic or product position.

We have a great deal of experience in executing strategic transactions, and we view this as a core competency. The company that we are today has come together through a number of significant transactions over the past two decades.

Across all of our businesses, our strategic focus continues to include creating opportunities to write more business through retaining and growing our relationships with our high-quality in-force accounts and bringing our franchise value to new customers. We will continue to seek to grow without compromising our return objectives or changing our risk profile, primarily by targeting customers, industries, products and geographies that we know well.

In terms of geography, we continue to believe that geopolitical risk and economic instability around the world are underappreciated. Accordingly, we like our North America concentration. That is not to say that we do not continue to recognize value and evaluate opportunities outside of North America, but we have set an even higher bar for those opportunities today.

More about business strategy & competitive advantages

Approach

At Travelers, our simple and unwavering mission for creating shareholder value is to deliver superior returns on equity by leveraging our competitive advantages; generate earnings and capital substantially in excess of our growth needs; and thoughtfully rightsize capital and grow book value per share over time.

Competitive advantages

Our competitive advantages serve as the foundation of our financial success and help us fulfill our promise to protect our customers.